They’re not content with just controlling our fiat money and your Bitcoin on centralized exchanges, so they’re coming for our self-custodied Bitcoin as well.

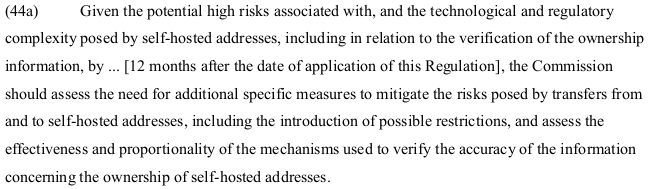

In a proposal to the European Union, the General Secretariat laid out an updated set of restrictions on cryptocurrency usage within the EU. While much of the proposal should be familiar, the updated language and recommendations around so-called “self-hosted wallets” are a frightening step towards tighter control over how we use Bitcoin. This new regulation proposes not only an implementation of the “Travel Rule” (requiring personal identification attached to each transfer between centralized, regulated entities) but also a limit of €1,000 to transfers from and to regulated exchanges and a recommendation to “mitigate the risks posed by transfers from and to self-hosted addresses” with forthcoming recommended restrictions.

One of the most onerous aspects of this new regulation is the introduction of a new phrase to imply that money that you own and control can and should be regulated by introducing the term “self-hosted,” when no such term exists for physical cash or fiat. When you choose to control your Bitcoin, you don’t have to “self-host” anything, you simply have the key to certain Bitcoin outputs and can transfer ownership of Bitcoin outputs (or coins) to other entities by signing over control to them. This key is a randomly generated 64-character string of letters and numbers (i.e. E987…3262), and regulating knowledge of a string of characters is an unbelievable overstep of power. The ability to transfer monetary value in a peer-to-peer manner is one that has existed since the early days of civilization and has historically been private, without requiring disclosure or surveillance.

The implication that the only way the State can prevent crime is by surveilling and collecting personal information from every financial transaction is an unprecedented shift towards centralized control. This control has not been necessary in the past for a safe, effective, and high-functioning society to prosper. When compared to fiat, cryptocurrencies like Bitcoin present an infinitesimally small amount of illicit activity. In their 2022 “Crypto Crime Report”, Chainalysis estimated that only 0.15% of all cryptocurrency volume involved illicit activity, compared to an estimated 2-5% of all GDP ($1.6-4 *trillion*) for fiat. The EU wishes to wield irrational fear and literary propaganda to justify centralizing and expanding their control over our lives.

With these numbers in mind, why are regulators like the EU attempting to tighten the noose on cryptocurrency usage by sovereign individuals? It certainly is not to prevent rampant crime, as cryptocurrencies are barely utilized for that and the low-hanging fruit is fiat use in crime. Is it for our own benefit? It certainly isn’t for our monetary safety, as users’ funds are far safer when self-custodied than when left to centralized exchanges and regulated custodians. Maybe, just maybe, they want to limit the ways in which each one of us can take back some control of our money from the state.

When they can’t control or surveil our finances or our actions, the power returns to the sovereign individual.